If The Government Shuts Down, Will It Change The Near-Term Outlook For US Fiscal Risk?

By James Picerno | The Milwaukee Company

Shutdown risk looms starting October 1 amid a fragile backdrop for government finances

The budget deficit and gold are signaling rising anxiety for the fiscal outlook

Bipartisan gridlock raises odds of no deal ahead of today’s midnight deadline for passing a new spending bill

There’s never a good time for a government shutdown, but if one starts tomorrow (Wed., Oct. 1) it arrives at a relatively vulnerable period due to a growing federal debt burden.

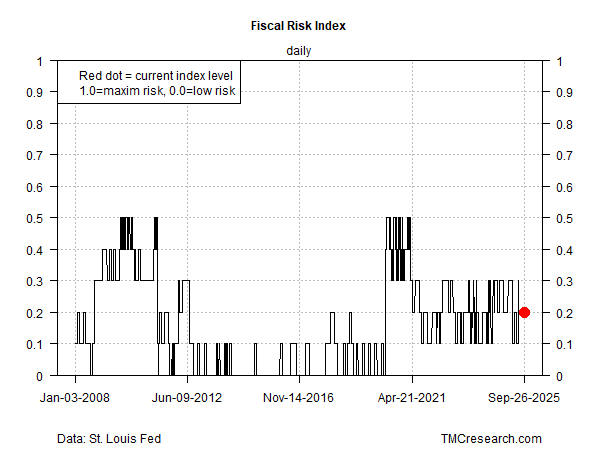

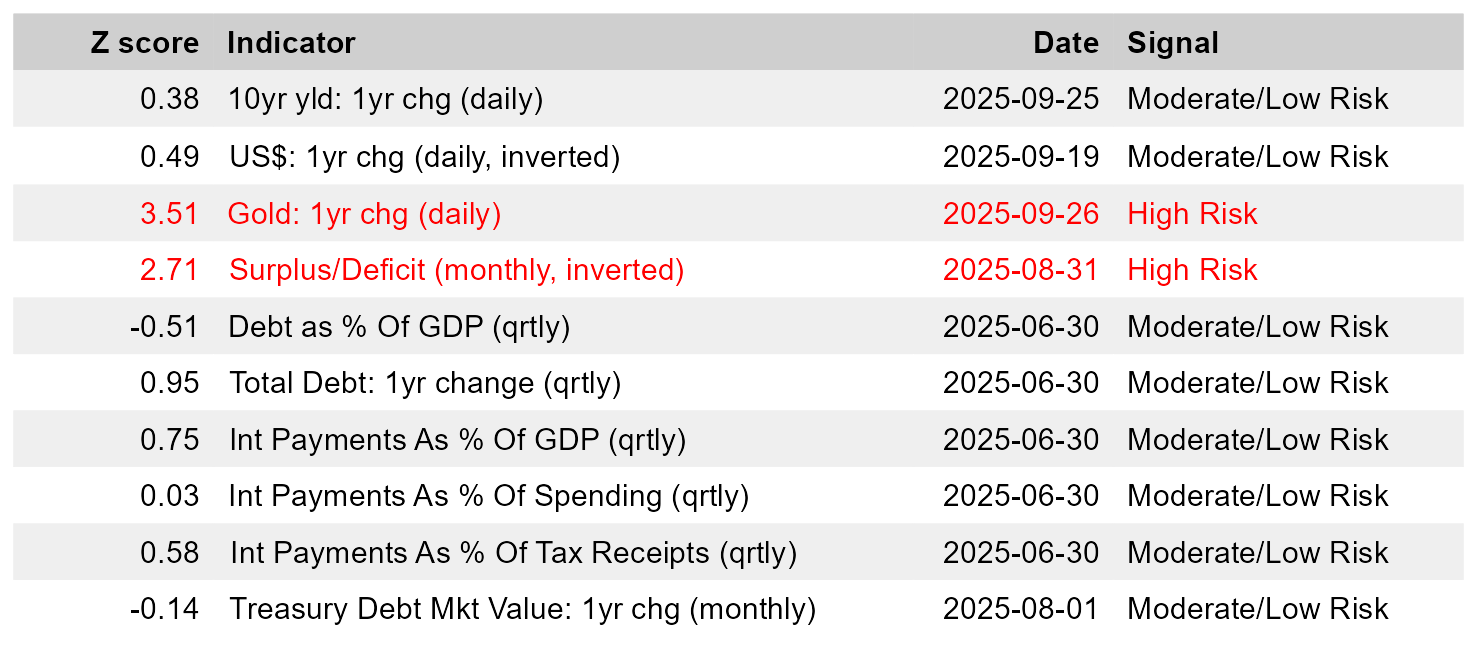

Fiscal risk has been stable lately compared with recent history, based on TMC Research’s model, which is designed to track how the overall macro and financial profile changes. On that score, the risk level remains in line with the past several years through Sep. 26.

The main outliers warning of trouble at the moment: a surge in the price of gold and the August update on the federal government’s surplus/deficit via the Treasury statements (the budget shortfall fell to its deepest shade of red ink in nine months). On both fronts, the latest changes are outliers that indicate elevated anxiety. The rest of the field continue to print in their respective ranges that have prevailed lately, based on changes measured in z-scores.

The pressing question this week: Will a government shutdown change the fiscal risk profile? The short answer: It doesn’t help, in part because it’s another, if temporary, headwind for economic activity.

“In stable times, this is not a particularly big deal,” says Marc Goldwin, senior vice president and senior policy director at the Committee for a Responsible Federal Budget, a think tank. “It’s probably a little bit of a bigger deal now.”

A shutdown would reduce economic activity, but only slightly. For example, Moody’s Analytics estimated that the 16-day federal shutdown in 2013 reduced GDP in the fourth quarter that year by one-half of a percentage point. “Federal and consumer spending are the biggest casualties, but international trade, housing and business investment were also disrupted,” the firm wrote.

The key variable is how long a shutdown lasts. A widely cited rule of thumb is that each week of a government shutdown reduces GDP by 0.2 percentage points.

Another crucial factor is the reaction in financial markets, the bond market in particular. A time of rising government debt, a high cost for debt servicing is a non-trivial affair. For the moment, yields remain low relative to recent history. The US 10-year Treasury yield closed down yesterday (Sep. 30) at 4.14%, near the low end of this year’s range.

Whatever the impact from a shutdown, it’s expected to be temporary, leading to a bounce-back in some degree after the government reopens.

A more immediate risk is the loss of economic releases. If a government shutdown arrives, the closure will postpone this Friday’s payrolls report for September. The Bureau of Labor Statistics issued a notice advising that “BLS will suspend all operations” if funding stops as of Oct. 1. “Economic data that are scheduled to be released during the lapse will not be released… The BLS website will not be updated with new content or restored in the event of a technical failure during a lapse.”

Inflation data could also be affected, depending on how long a shutdown lasts. The BLS publishes monthly updates of the Consumer Price Index (CPI) – the September report is scheduled for release on Oct. 15.

The Federal Reserve is already struggling to set monetary policy at a time of elevated uncertainty about the path of inflation and the labor market. Removing key data points from the analysis raises the risk, if only marginally, of a policy error for the next Fed meeting on Oct. 29.