Hints Of Stagflation Complicate The Fed’s Next Decision On Interest Rates

By James Picerno | The Milwaukee Company

A softer-than-expected payrolls report for July suggests the labor market is slowing, but…

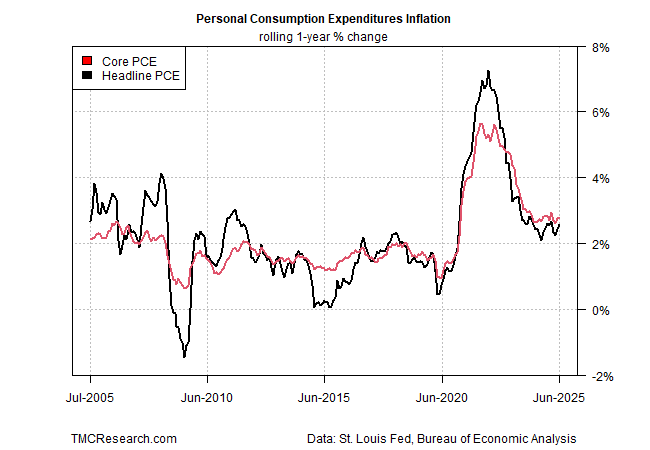

The Fed’s preferred inflation gauge continued to edge higher in June

The Fed is expected to cut rates at the next policy meeting on Sep. 17

For a second month in June, the Federal Reserve’s preferred inflation gauge edged higher in year-over-year terms. Although the modestly firmer trend is still middling relative to recent history, the back-to-back increases may be a factor in persuading the central bank to again forgo a cut in interest rates at the next policy meeting on Sep. 17.

Payrolls data released for July, by contrast, point to an ongoing slowdown in hiring. The economy added just 73,000 jobs last month – well below the consensus forecast. In addition, the Bureau of Labor Statistics issued substantial downward revisions to the previously reported employment figures for May and June, reducing those two months’ combined job gains by 258,000. While July’s headline increase is weak, it also reflects a modest rebound in hiring momentum after the near-stagnant change in payrolls in May and June. Nonetheless, the year-over-year rise in nonfarm payrolls was fractionally below the 1% mark for a second month – the softest since the pandemic.

Conflicting data for inflation and payrolls complicate the Fed’s mission to satisfy its dual mandate: maintain stable prices and maximize employment. Although there’s still room for debate about whether inflation is rebounding, or if hiring will continue to slow, President Trump’s revised tariff policy could complicate the central bank’s decision process.

On Thursday, the President announced new tariffs on dozens of countries. He signed an executive order that revised “reciprocal” import fees with new levies ranging from 10% to 41% that are set to start from Aug. 7.

The question is whether higher tariffs will lift inflation, dampen economic growth, both — or neither — in the months ahead?

At the moment, the market seems to be leaning into the slower-growth view as the bigger risk. The US 10-year Treasury yield fell sharply on Friday, dropping to 4.22%, the lowest since April 30. Fed funds futures are now pricing in a high probability (roughly 88%) of a rate cut at the September 17 FOMC meeting. By some accounts, the possibility of a ½-percentage point cut is a possibility in the wake of the July payrolls data, although the consensus still leans toward a ¼-point cut.

Despite the softer pace of hiring last month, other employment indicators still paint a healthy jobs market. Notably, initial jobless claims – a leading indicator for payrolls – continue to print at a low level and imply that the labor market remains healthy.

Perhaps a decisive factor will be the upcoming consumer inflation data for July, due on Aug. 12. The annual change for the Consumer Price Index (CPI) rose for a third straight month in June to 2.7%. Although that’s still within the middle of the range in recent history, another increase in the annual pace would be tougher for the Fed to ignore.

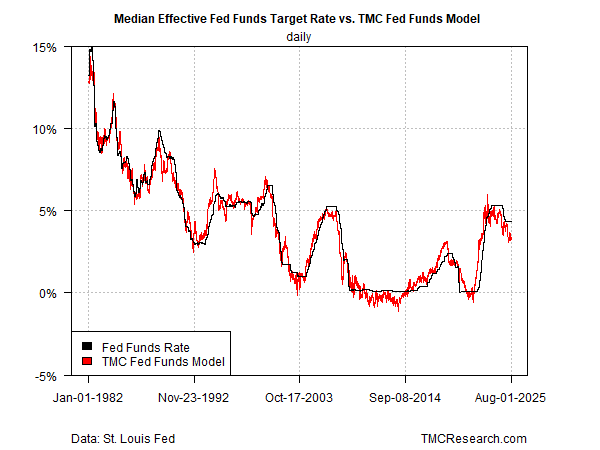

Meanwhile, TMC Research’s Fed Funds Model continues to indicate that monetary policy remains moderately tight: the estimated optimal rate for policy is now more than a full percentage point below the current median 4.33% Fed funds target rate. The current stance implies a strong case for rate cuts, but much depends on whether the central bank sees inflation or slower growth in payrolls as the bigger threat.

For now, policymakers appear to be proceeding with caution, shaped in part by past criticism that they were too slow to tighten policy when inflationary pressures first surfaced in 2021.

The Treasury market is leaning toward the slower-growth outlook as the main concern. The policy-sensitive 2-year yield fall sharply on Friday to 3.70%, the lowest since May – and well below the current 4.25%-to-4.50% Fed funds target range. The not-so-subtle implication: the bond market is confident that a rate cut is imminent.

The incoming data between now and the Fed’s Sep. 17 look set to be decisive for determining how the central bank interprets the recent run of mixed economic data. The softer jobs data appears to have the upper hand at the moment for influencing the market. The question is whether next week’s CPI data will change the calculus?