Gold and Silver Shine Brighter Together

By James Picerno | The Milwaukee Company

Silver has outperformed gold by a wide margin recently

Silver’s role as a portfolio diversifier compliments gold’s role as a hedging asset at times

Industrial and tech demand for silver may give the metal an edge over gold in years ahead

Silver has historically played second fiddle to gold in the horse race of precious metals, but this year silver is in the spotlight by outperforming its rival.

Silver’s trend, to put it bluntly, has been white hot lately -- the metal recently surged to its highest level in 14 years before pulling back over the past week. For the past three months, silver is up nearly 15% whereas gold is down slightly. Analysts cite several factors for the rally:

Silver has been priced at a significant discount to gold in recent years, according to some commodities analysts, which suggests silver has been a more affordable alternative gold. One measure of relative valuation is the gold-silver ratio, which rose to a five-year high in the spring, implying that gold’s premium vs. silver has been elevated. (The premium has since fallen and is again at a middling level relative to the past two years.)

Industrial demand for silver has outpaced supply in recent years, and several forecasters expect the gap to persist for the near term if not longer.

A bullish factor for silver demand arises from various technology applications. The metal is a component in solar panels, smart phones, electric vehicles and leading-edge medical and healthcare innovations. As these and other technologies witness wider use, silver demand could rise further.

Expectations that interest rates will ease in the near-term future is another plus for silver (and gold) because lower interest rates reduce the competitive allure of bonds, a “safe” asset alternative that overlaps with the role of precious metals in some degree.

Precious metals and asset allocation

Silver is a speculative commodity in its own right, but does it also deserve consideration for portfolio design? Gold has long been viewed as the dominant choice for tail-risk hedging (providing ballast if stocks and/or bonds tumble), but silver’s role is less widely discussed. For some context on how silver compares with gold for asset allocation, TMC Research ran the numbers.

The main conclusion: silver exhibits valuable behavior from a diversification standpoint, even in comparison with gold. Although each of the metals are useful for diversifying portfolios, there are times when silver rallies are distinct from gold’s – an attribute that inspires a closer look.

To kick the tires, we analyzed a pair of exchanged-traded portfolios that own their respective metals directly: SPDR Gold Trust (GLD) and iShares Silver Trust (SLV). The results below compare the two funds, including how they influence a simple 60/40 stock-bond portfolio.

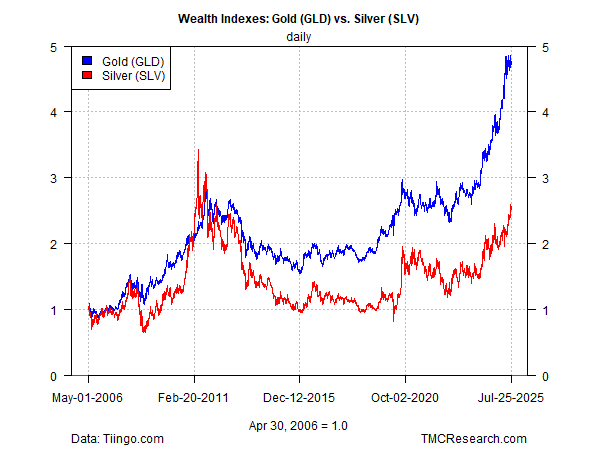

Let’s start by comparing silver with gold as standalone investments. As the first chat below shows, gold (GLD) has been the clear winner over silver (SLV) for the past two decades.

It’s tempting to conclude that gold’s the preferable choice, but there are times when silver outperforms. Over the past three years, for instance, SLV has earned nearly 150 basis points more than gold in annualized terms. (Note: all returns shown below that are longer than 1-year are annualized.)

Consider, too, that gold and silver generally exhibit a degree of independence from one another. The daily return correlation for GLD and SLV is 0.79 since 2006, which reflects a moderate degree of price autonomy against each other. (1.0 indicates perfect positive correlation, 0 is no correlation.)

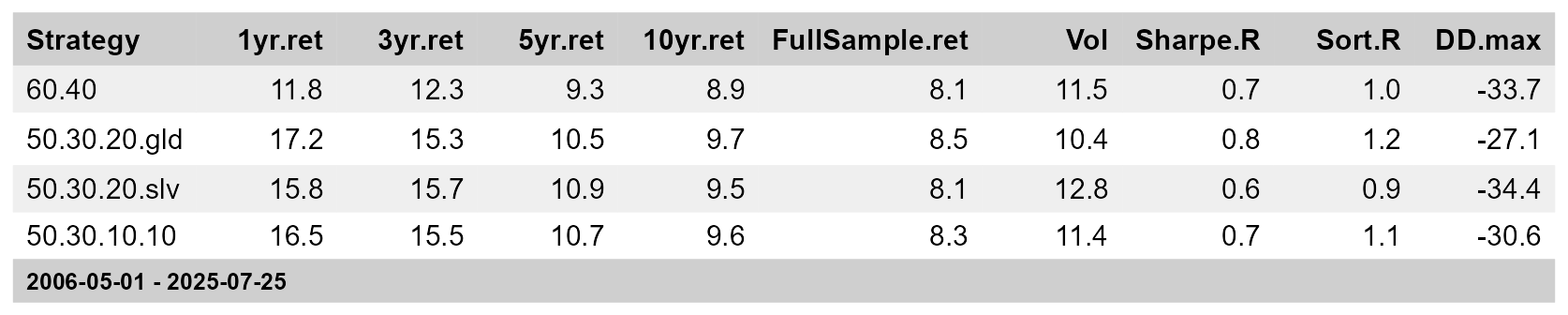

To assess how silver and gold interact within a conventional investment portfolio, we analyzed the data as follows. First, create a benchmark sans both metals: a 60/40 stock/bond portfolio (60.40 in table below), based on a pair of ETFs: SPDR S&P 500 (SPY) and iShares Core US Aggregate Bond (AGG). Next, alter the 60/40 mix with a 20% gold allocation, financed by reducing stocks to 50% and bonds to 30% (50.30.20.gld). The same silver-only allocation is shown for the 50.30.20.slv portfolio. Finally, we created a portfolio with stocks, bonds, silver and gold, with target weights of 50%, 30%, 10% and 10%, respectively (the 50.30.10.10 strategy). All portfolios have start dates of May 1, 2006 start dates and are rebalanced to target weights at the end of each calendar year.

For the full sample period (since 2006), the portfolio with stocks, bonds and gold (50.30.20.gld) topped the performance race, albeit only mildly so. This portfolio’s risk-adjusted return (Sharpe ratio) is also the highest since 2006, but not dramatically. (All risk metrics reflect data since 2006.)

A closer look at the silver lining

Does that mean that gold’s the hands-down winner and we can ignore silver? Not so fast. First, silver’s influence in recent years is superior for asset allocation, as shown for the 3- and 5-year trailing windows. Gold, in other words, doesn’t always win the precious metals horse race.

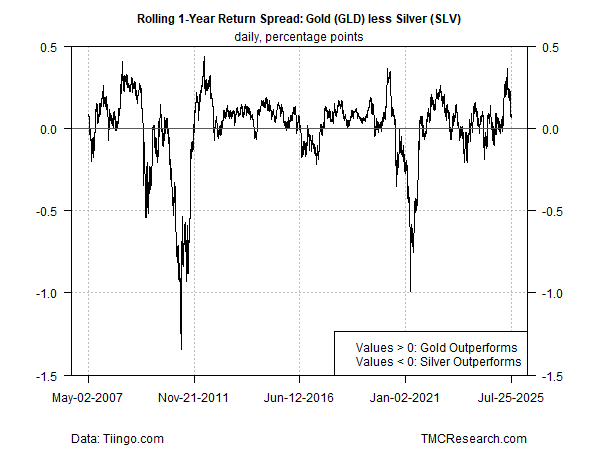

For a deeper dive, the next chart calculates the excess return for gold vs. silver via the rolling 1-year return spread. When the line is above zero, gold is outperforming over the previous year, and vice versa. Gold tends to win most of the time, but there are some notable exceptions, including two extreme periods when silver’s edge was hefty.

Silver beat gold by a wide margin at times in 2009 and 2010, following the financial crisis in 2008. Silver also left gold in the dust during the early months of the pandemic shock.

The implication: silver’s tail-risk-hedging attributes vis-à-vis gold are sometimes complimentary, which suggests that gold and silver can both play productive roles in diversifying conventional portfolios of stocks and bonds.

Exactly when silver shines brighter than gold, or vice versa, is impossible to know in advance, although monitoring price trends can help in developing tactical forecasts for deciding when to favor one metal or the other.

Another solution, which is forecast free and immune to timing mistakes: routinely hold gold and silver.

As the table above suggests, adding silver to a mix of stocks, bonds and gold may incur an opportunity cost at times, but it’s been slight for the past two decades, at least for the weights used in our test. But it’s also true that silver can be a timely hedge when gold’s value as a diversifier is in remission.

Holding both metals to hedge some forms of tail risk for stocks and bonds, in other words, looks like a reasonable strategy for the long run, as opposed to betting that either metal alone will always outshine the other.