Geopolitical Tension Pressures Stocks, While Earnings Still Offer Support

By James Picerno | The Milwaukee Company

Stocks are down, but earnings help cushion the blow

War pressure is rising, but earnings forecasts remain upbeat

The longer the war lasts, the greater the risk that earnings could stumble

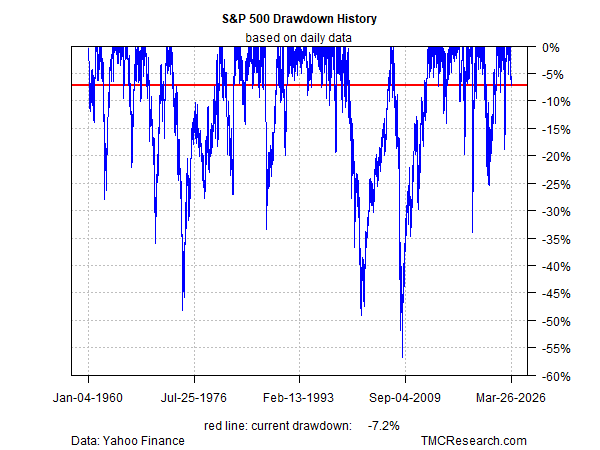

The stock market’s decline since the Iran war started isn’t surprising, but some market observers have been puzzled by the gradual, orderly slide in equities to date. Why hasn’t the conflict triggered a deeper correction? Robust earnings may be a factor.

The S&P 500’s current drawdown is -7.2%, which is still relatively modest by historical standards. No one knows if the decline will deepen, or when the war will end, but solid earnings data is a likely reason why the correction, so far, is still within a “normal” range.

Earnings are a key—if not the primary—driver of equity returns through time, which suggests that recent gains on this front, along with upbeat expectations for the near‑term outlook, may have helped limit the downside for stocks.

The research firm FactSet estimates that the equity market’s year‑over‑year earnings growth rate through this year’s first quarter is 12.5%. “If 12.5% is the actual growth rate for the quarter, it will mark the sixth straight quarter of double‑digit (year‑over‑year) earnings growth reported by the index,” writes the senior analyst.

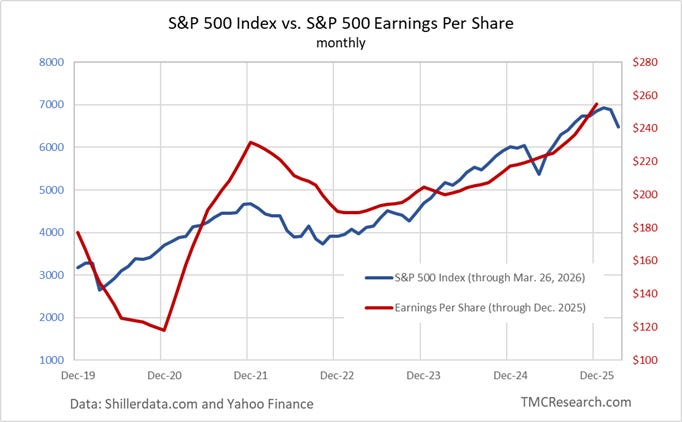

For recent historical perspective, consider the stock market’s performance (S&P 500 Index) in context with earnings. Unsurprisingly, equities have been rising in line with earnings growth. If the bullish forecasts for earnings are accurate, the growth trend may provide support for stocks and help minimize the war-related downside risk.

Market volatility in the short term can spike for a variety of reasons, and so it’s never clear how much support earnings can provide over a few weeks or months. As the renowned value investor Ben Graham famously observed, “In the short run, the market is a voting machine, but in the long run it is a weighing machine.”

Wall Street remains generally upbeat on S&P earnings for 2026. The question is how much of a haircut could brewing if the war runs longer than the optimistic views suggest?

Analysts at Barclays this week wrote: “We believe the US continues to offer stronger nominal growth than other major economies and a secular growth engine in technology that shows few signs of stopping,” the bank’s strategists advised. “We are incrementally bullish on US equities, though the road likely stays bumpy until we turn a corner.”

The war is still the elephant in the room in terms of risk factors. The sooner the conflict ends, the higher the confidence that the growth trend for earnings can continue with minimal damage.

Another key variable to watch is economic growth. The Atlanta Fed’s current nowcast for the upcoming first‑quarter GDP report points to a moderate rebound in output following the sluggish rise in the fourth quarter.

If the war ends soon, and the economic headwinds from the conflict are relatively mild and short-lived, the odds will remain favorable that corporate earnings will continue to rise and provide a degree of ballast for the market in the months ahead.