Foreign Stocks Are Crushing US Equities This Year. A Weak US Dollar Is A Factor

By James Picerno | The Milwaukee Company | jpicerno@themilwaukeecompany.com

Global equities ex-US are up nearly 9% year to date vs. a 4.3% decline for American shares, based on a set of ETFs.

The correction in the US dollar in 2025 is a factor for the outperformance in foreign stocks.

History suggests that the US dollar and the return spread for US stocks less foreign equities is moderately correlated and therefore useful as a first approximation for estimating near-term return expectations.

Foreign stocks have been outperforming US equities by a wide margin year to date. There are several key factors driving the rally in global equities ex-US, including the slide in the US dollar relative to foreign currencies.

From the perspective of a US-based investor, a weaker dollar equates with stronger performance for foreign stocks, all else equal. The opposite is also true: When the greenback strengthens, foreign assets tend to suffer vs. US shares. It’s not a perfect relationship by any means, nor is it the only one for evaluating the outlook for US vs. foreign shares. But the forex factor can be a powerful tailwind, or headwind, depending on which way the wind is blowing in currency markets. Monitoring the dollar’s trend, in other words, is a crucial part of managing a global portfolio’s asset allocation.

At the moment, the wind is blowing in favor of foreign currencies, which in turn is partially helping stock markets outside the US outperform their American counterparts by a wide margin. Using a set of proxy ETFs tells the story: Vanguard Total International Stock Market ETF (VXUS) is up 9% this year vs. a 4.3% decline for SPDR S&P 500 ETF (SPY), a benchmark for American firms, through mid-day trading today (Mar. 18). The gap is striking after two straight calendar years of strong outperformance by the US market.

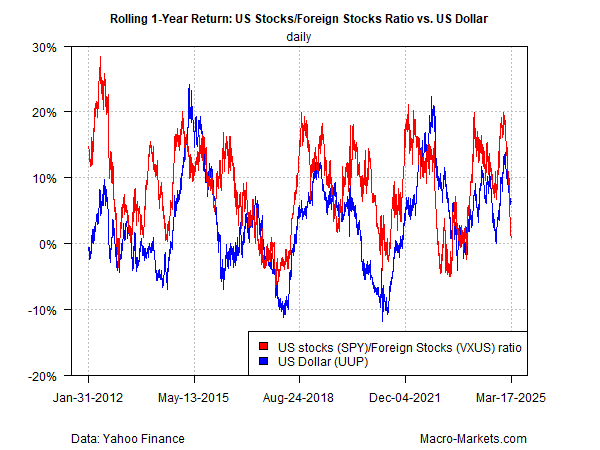

Although equity returns are driven by multiple factors, forex risk appears to be a significant influence for foreign stocks this year. For some perspective on how the forex influences ebbs and flow, consider the first chart, which shows the rolling 1-year changes for the US dollar (based on an ETF with ticker UUP) vs. the ratio of US stocks (SPY) to foreign stocks (VXUS). The correlation between the two indexes is moderately positive (posting a correlation of roughly 0.5 since 2012). The relationship more or less holds for shorter rolling periods. The point is that the dollar’s trend bias casts a non-trivial influence on foreign stocks relative to US shares.

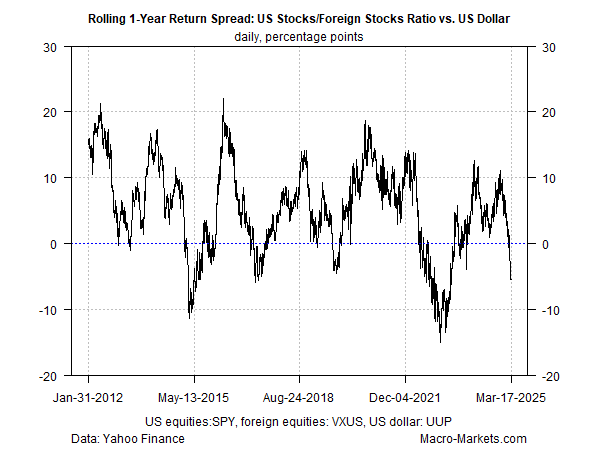

For another view, the second chart tracks the spread between the two time series in the first chart. When the 1-year return spread is above zero, US equities are outperforming their foreign counterparts, and vice versa. The main takeaway: there’s a short-to-medium-term cycle for the relative outperformance for US and foreign stocks vs. the US dollar.

Notice the tendency at times for the spread to reverse relatively sharply after it peaks or troughs. Although the timing or speed of reversals can’t be reliably predicted, the historical record suggests periods when the odds of a countertrend kicking in appear elevated.

With the benefit of hindsight, one of the periods of an elevated spread arrived in late-2024, when the SPY/VXUS ratio rose to a relatively lofty level. Although that alone didn’t ensure that foreign stocks would outperform US shares this year, it was a clue that suggested last year’s widening gap in favor of American shares – a gap that accelerated in the final months of 2024 – had reached an unsustainable level that would soon peak.

History suggests the tide can go to extremes, leading to a strong countermove, as the sharply falling (and now negative) spread in the second chart suggests. No one knows when gravy train of foreign equities writ large will run out of fuel that powers their bull run, but monitoring the dollar’s trend offers a reasonable first step for managing expectations and, perhaps, adjusting asset allocation when a given trend appears to have gone too far.

Read a pdf version of this article: