Forecasting Bond Fund Returns In A Post-2021 Regime Isn’t Getting Any Easier

By James Picerno | The Milwaukee Company

The recent shift from a decades-long decline in yields to rapid rate hikes has increased the difficulty and uncertainty in developing return expectations for bond funds

Bond funds, due to their structure, introduce substantial return variability and complexity, causing their performance to often deviate significantly from simple yield-based forecasts.

Individual bonds held to maturity, by contrast, offer relatively reliable, predictable returns that closely match the current yield at the time of purchase.

Developing reliable return expectations for bonds is straightforward, at least compared with the far greater uncertainty associated with stocks. But the relative reliability for projecting performance with fixed-income securities is closely linked to buying and holding a bond through its maturity date. Results over shorter periods can and often do vary substantially. Investing in bond funds introduces more return variability vs. the implied outlook with a relevant buy-and-hold position in an individual Treasury security or corporate bond.

A high degree of clarity for expected return with bonds is a function of using the current yield at the time of purchase as a forecast. For example, a 5-year Treasury Note is currently trading around 3.7%. Assuming you purchase the security directly at that current yield, and hold it through maturity, the performance will roughly match the yield at the time of purchase. (Technically, yield-to-maturity, which factors in additional variables, is a more accurate measure for projecting return, but for simplicity in this illustration let’s assume current yield is equivalent. Note, too, that we’re ignoring such issues as how you invest a bond’s payouts through time and other variables, such as callable bonds and defaults that affect returns for corporates.)

Investing in bonds by way of a fund adds another layer of complication that can and usually does affect performance, sometimes in ways that aren’t intuitive. As an example, consider a buy-and-hold investment in Vanguard Total Bond Market Index Fund (VBMFX), a popular mutual fund that holds investment-grade securities.

Morningstar reports that a bit more than half of VBMFX’s portfolio is held in US government bonds, with corporates (25%) and securitized bonds making up most of the rest (22%). The fund’s yield to maturity is 4.38%.

Assume the 5-year Treasury yield is a proxy for the fund, which implies that when you bought VBMFX the current 5-year rate is a reasonable first approximation of what you can expect to earn over the next 5 years. The broader portfolio holdings in VBMFX will create differences vs. a 5-year Note, but current yield for the government security should be a decent back-of-the-envelope forecast.

Sometimes that’s a reasonable assumption, but it can also be wide of the mark. Much depends on current macro conditions and the outlook when you buy VBMFX.

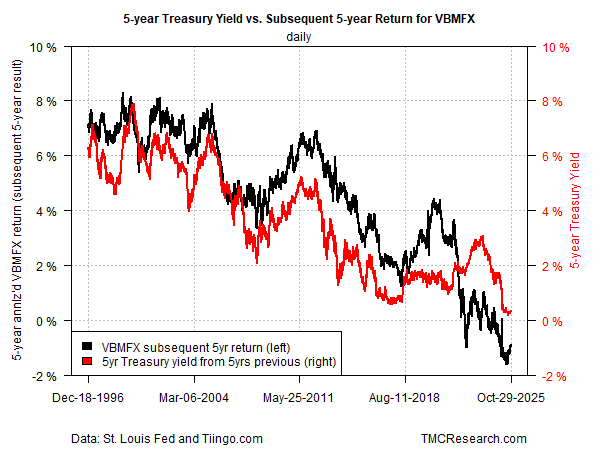

For context, the chart below compares the 5-year annualized total return for VBMFX five years hence relative to the 5-year yield. If the 5-year yield was a perfect forecast for VBMFX’s return five years down the road, the two lines would match exactly. Clearly, that’s not the case. Although there are periods when the 5-year yield (red line in chart) is a reasonably accurate estimate of the future 5-year return for VBMFX (black line), there can be substantial divergences for prolonged periods.

For most of VBMFX’s history, the fund has outperformed or matched the 5-year yield. But since the Federal Reserve’s latest round of rate hikes starting in 2022, VBMFX’s five-year return has trailed the 5-year yield (from five years earlier) by a relatively wide margin for an extended period.

There are several possible reasons for the mismatch in recent years, including the rapid pace of 2022-2023 rate hikes, the lingering effects of the pandemic on the economy, and the sharp spike in inflation in 2022-2023.

Another relevant factor: the four-decade trend of generally declining interest rates that ended in 2021. Forty years of falling yields bred a high degree of comfort in assuming that risk was minimal for the bond market’s outlook. When that regime ended, the shift introduced more uncertainty and volatility into the market to a degree unseen in decades.

Even before 2021, it was unsurprising that VBMFX’s rolling 5-year return deviated from the implied forecast via a 5-year yield. The fund, although it tracks an index, holds a range of bonds and therefore takes more risk vs. a Treasury note. The higher risk mostly paid off, until the 2022 rate hikes.

The larger point is that developing return and risk expectations for bond funds has become considerably more nuanced. By contrast, forecasting VBMFX and other bond strategies was more or less pro forma in the pre-2021 era, with relatively low stakes, given the general slide in yields.

That era ended in 2022, and it’s debatable when or if it will return. Between tariffs, gridlock in government, elevated fiscal risk for the US government, and the potential for AI-fueled economic disruption, a repeat performance of the secular slide in interest rates during 1981-2021 looks unlikely, at least at the moment.

In turn, the stakes are higher for crunching the numbers and reading the trends for developing expectations for bond funds.

Buying and holding a Treasury note, by comparison, still offers simplicity and relative reliability for projecting future performance.