Fed Monetary Policy Remains Tight As It Waits For Tariff-Related Inflation Signals

By James Picerno | The Milwaukee Company

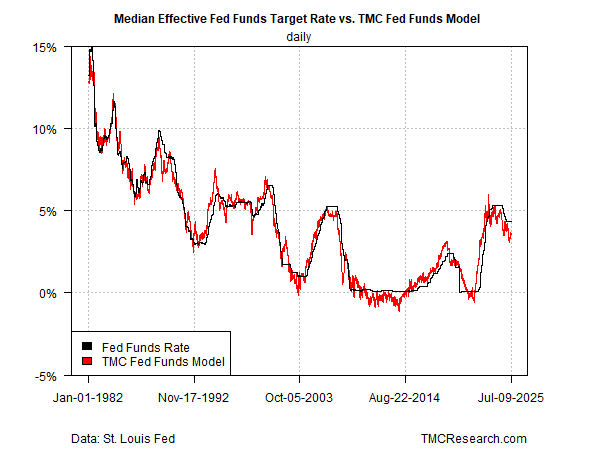

The Fed’s median target rate is still well above the annual pace of US consumer inflation.

The odds are low that the Fed will cut rates at the upcoming July 30 policy announcement.

Our Fed model estimates that the current median Fed target rate is nearly ¾ percentage point above the neutral rate, based on the current state of US macro conditions.

President Trump’s latest announcement on tariffs earlier this week will likely reinforce the Federal Reserve’s preference to keep its target rate steady at this month’s monetary policy announcement on July 30.

On Monday, the President delayed imposing higher tariffs on US imports. He sent letters to 14 countries (and expanded the list on Wednesday) – including two of America’s biggest trading partners, Japan and South Korea – and advised that that new levies of at least 25% would start on August 1 without a trade deal. The letters arrived ahead of the previously announced July 9 deadline for higher tariffs.

The announcement extends the tariff deadline, but provides little, if any, new clarity on how US trade policy could change in the weeks ahead. As a result, the Federal Reserve’s near-term plans for policy will likely continue, namely: Keeping rates steady until the tariff-related inflation outlook becomes clearer.

The status quo translates to keeping monetary policy moderately tight. The current median 4.33% for the central bank’s target rate remains well above the 2.8% year-over-year pace of US core consumer inflation and the 2.4% rise in headline inflation vs. the year-ago level.

TMC Research’s multi-factor Fed funds model also indicates that policy remains moderately tight. By our estimate, the current median Fed funds target rate is 71 basis points above our estimate of the neutral rate – fractionally higher vs. our previous update on June 16.

Another reason the Fed appears comfortable with leaving rates unchanged is the resilient labor market, which provides a rationale for asserting that half of the central bank’s dual mandate – stable prices and maximum employment – is satisfied. In June, the unemployment rate ticked down to a modest 4.1% in June and payrolls rose 147,000, beating expectations. In both cases, the results are line with the range in recent history, which provides support for the Fed to argue that hiring remains healthy and so rate cuts aren’t necessary.

Initial jobless claims – a leading indicator for payrolls – also paint an upbeat outlook. After running higher through early June, weekly filings for unemployment benefits pulled back and have fallen in each of the past three weeks through June 28. Claims are posting a decline vs. the year-ago level for the first time since March, which suggests that the near-term outlook for the labor market has improved.

Meanwhile, market sentiment today continues to price in no change in rates for the upcoming July 30 policy meeting and a moderately high probability (roughly 70%) for a rate cut in September, based on Fed funds futures via CME Group data.

The policy-sensitive US 2-year yield is dispatching a similar forecast. This maturity traded down on Wednesday, dropping to 3.85%, which is well below the median 4.33% Fed funds rate. The relatively low yield is another dovish market-based forecast for the Fed target rate’s path.

Next week’s June report of US consumer inflation (Tuesday, July 15) isn’t expected to change the calculus. TMC Research’s modeling points to a comparable or fractionally higher year-over-year change in the core Consumer Price Index (CPI) relative to the trend in May.

Given the consensus that the Fed will remain on hold for the July 30 FOMC meeting, the real test awaits at the September 17 policy announcement. By then, another payrolls report, and two additional CPI updates, will be in hand.

Meanwhile, markets are pricing in cuts for the near term. There’s also increasing political pressure from the White House in favor of cuts. But without a clear rise in inflation between now and September 17, the Fed will be hard pressed to keep policy steady.