Fed Expected To Hold Interest Rates Steady At Wednesday’s Policy Meeting

By James Picerno | The Milwaukee Company | jpicerno@themilwaukeecompany.com

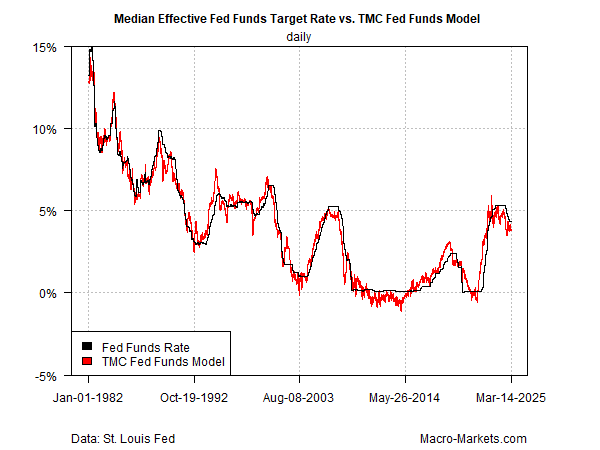

TMC Research’s Fed funds model anticipates no change in the central bank’s target interest rate at this week’s policy announcement on Wednesday, Mar. 19.

The Federal Reserve’s target rate remains in line with a neutral stance, based on TMC Research’s Fed funds model.

Although the Fed is unlikely to change interest rates this week, it’s on high alert for higher inflation, softer economic activity unfolding at the same time – stagflation risk.

Consumer inflation slowed in February, which potentially gives the Federal Reserve more leeway to leave its target rate unchanged when it announces its revised policy stance this week (Wed., Mar. 19). But last month’s data is ancient history at a time of rapidly escalating tariffs and so uncertainty has increased about how the Fed will manage policy in the weeks and months ahead.

The challenge is especially complicated for monetary policy because the threat of higher inflation may accompany softer economic growth, at least in the short, due to higher tariffs.

The Fed is on high-alert for new inflationary pressures, but the numbers available to date aren’t particularly useful for assessing tariff-related inflation risk, which will take weeks if not months to register a clear signal in the economy.

Fed funds futures today are pricing in a near-certain probability that the Fed will leave its target rate unchanged at a 4.25%-to-4.50% range on Wednesday. The market’s estimate for keeping rates unchanged falls to a roughly 76% probability for the next FOMC meeting on May 7, but that estimate should be viewed cautiously since much depends on how the incoming data compares (and how or if tariff policy shifts) in the weeks ahead.

The President today reaffirmed that a broad US application of reciprocal and sectoral tariffs are still set to begin on Apr. 2.

While the near-term outlook for interest rates is steady, the Fed is potentially at risk of being caught between a proverbial rock and the hard place as two competing forces threaten to drive policy adjustments in opposite directions, at least in theory. As noted, the risk of higher inflation may be lurking in the near term due to escalating tariffs. If inflation does pick up, the shift implies tightening monetary policy will be appropriate.

Those same tariffs could also slow the economy, which would warrant cutting interest rates. Although there’s no compelling hard data at the moment that clearly shows a material softening in US growth, there’s a growing number of nowcasts and forecasts indicating that a downshift in some degree is likely, largely based on the view that tariffs will continue and perhaps expand as other countries respond. Google searches for the word “recession” have surged recently, which suggests that the unease about the economic outlook is starting to resonate in the public sphere.

Investors will be closely watching the Fed’s press conference on Wednesday for clues about how Chairman Jerome Powell and the board of governors are thinking about assessing risks for inflation and economic activity as it relates to the labor market. The Fed will also publish new economic forecasts, which will provide insight into the central bank’s revised expectations.

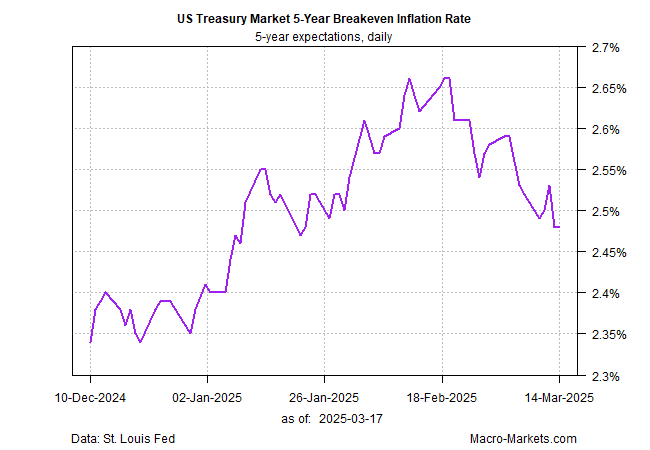

An encouraging real-time signal on the inflation front is the US Treasury market’s ongoing downshift for inflation expectations, based on the 5-year breakeven rate, which is the spread for the nominal 5-year yield less its inflation-indexed counterpart. As of Friday (Mar. 14), the spread was steady at 2.48% after peaking in mid-February at 2.66%.

Encouraging, except that worries about economic activity may be driving inflation expectations lower. In that case, the Fed may soon feel compelled to cut rates if the economic-weakness factor dominates.

For the moment, a wait-and-see attitude prevails among policymakers. Managing expectations for how the central bank’s policy pivots, or not – and which way it pivots – will be top of mind for markets for the foreseeable future. Powell, in turn, may face his biggest policy challenge yet in his tenure – a challenge that starts with Wednesday’s press conference.

Read a pdf version of this article: