Fed Cuts Its Target Interest Rate And Signals More to Come

By James Picerno | The Milwaukee Company

Treasury yields rise after Fed rate cut amid lingering inflation concerns

Fed Chair Powell flagged labor market slowdown as higher priority over inflation

Tariff uncertainty is still a risk factor for inflation

US Treasury yields rose across the yield curve on Thursday, a day after the Federal Reserve cut its target rate for the first time this year. The biggest increases were at the longer end of the curve, which is more sensitive to inflation risk.

The increase in market rates suggests lingering investor concern that inflation will remain well above the Fed’s 2% target, in part because softer monetary policy could make it harder to close the gap in the near term.

In yesterday’s press conference, Fed Chairman Powell recognized that “We have begun to see goods prices showing through into higher inflation, and actually the increase in goods prices accounts for most of the increase in inflation, or perhaps all of the increase in inflation over the course of this year.” He added that the effects for the economy “are not very large at this point,” although “we do expect them to continue to build over the course of the rest of the year and into next year.”

Taking a cautious view on the prospects that inflation will remain contained, much less fall, the US 10-year Treasury yield rose on Thursday to 4.11%, the highest since Sep. 4. The policy-sensitive 2-year yield also increased. Morningstar notes that it’s “highly unusual” for Treasury rates to rise so quickly after the Fed begins a rate-cutting cycle.

The path of least resistance is still down for the Fed target rate

The benchmark rate remains well below the previous peak in February (roughly 4.80%), and so yesterday’s pop in market yields could turn out to be noise. The case for expecting interest rates to slide further draws on several sources, starting with the Fed’s new projections. Members of the central bank’s policy-setting committee predict the median Fed funds rate will fall to 3.6% this year, slipping to 3.4% in 2026 from the current 4.13% median. Meantime, the Fed funds futures market is pricing in two more ¼-point cuts by the end of the year.

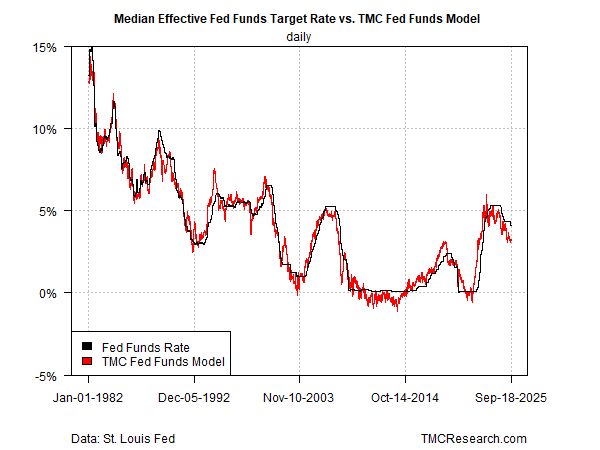

TMC Research’s Fed funds model also indicates space for additional policy easing. After Wednesday’s rate cut, our rough estimate of the neutral rate for the Fed’s target remains well below the 4.13% median – a gap that suggests policy remains relatively tight.

What isn’t factored into the model’s analytics, however, could turn out to be significant, namely: the effects of tariffs on inflation in the months ahead. Modeling this “soft” effect is challenging since it relies on guesswork rather than hard data.

One of the reasons, arguably the key reason, that the Fed has been slow to cut rates in recent months is the uncertainty surrounding how tariffs will affect pricing pressure and the economy. The extreme, rapid shift in US tariff policy this year has limited, if any, precedent in modern history for analyzing the effects.

One view is that inflation is only starting to edge higher from tariffs. If so, easing monetary policy could exacerbate a new reflationary trend. A conflicting theory is that tariffs will be a headwind for economic growth, if only on the margins—an effect that implies lower rates will be needed as an offsetting factor.

Powell was careful to hedge on the uncertainty issue, explaining on Wednesday that while inflation “remains somewhat elevated relative to our 2% longer-run goal,” the labor market is the higher priority at the moment because “payroll job gains have slowed significantly to a pace of just 29,000 per month over the past three months.” Notably, “labor demand has softened and the recent pace of job creation appears to be running below the “breakeven” rate needed to hold the unemployment rate constant.”

Still trading in a range

From an investment perspective vis-à-vis the bond market, a crucial question is when/if the 10-year yield breaks out of its recent range. At the moment, the bias still looks heavily skewed to the downside — the benchmark rate is trading near the bottom of its “normal” range, per the top chart below.

To the extent the 10-year rate moves to the upper range of the grey box, inflation concerns would be the likely catalyst. For now, at least, that risk is in remission. A key test of this relatively benign environment for bonds is next month’s September update for consumer inflation (Oct. 15).