Fed Chair Warsh Steps In as Inflation Reignites and the Treasury Market Hints at a Rate Hike

By James Picerno | The Milwaukee Company

Hotter inflation will feature at Warsh’s first policy meeting and press conference this month

His June 17 debut will reveal how he handles rising price pressure

The Treasury market hints at a rate hike in the near term

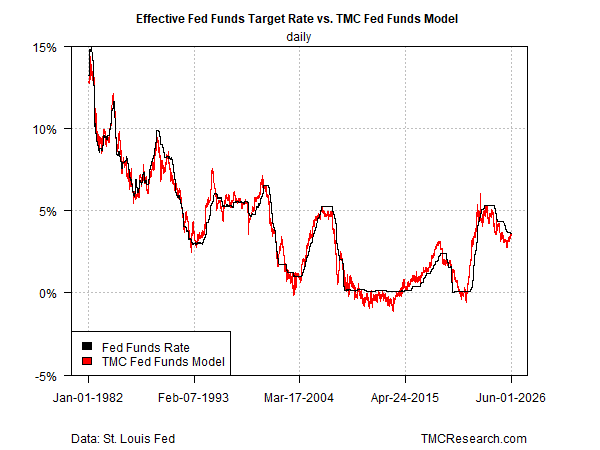

Federal Reserve Chair Kevin Warsh will preside over his first Federal Open Market Committee (FOMC) meeting later this month (June 16–17). Ahead of his public debut as the top central banker, monetary policy is essentially neutral for the first time in 2½ years, according to TMC Research’s estimate. Inflation, by contrast, is trending higher, which may set up an early challenge for the newly minted Fed chief.

Fed funds futures are still pricing in a near‑certainty that the Fed will leave its current 3.50%–3.75% target range unchanged this month, but the Treasury market is sending a different message for later in the year. The 2‑year Treasury yield — widely viewed as a proxy for policy expectations — is trading just above 4.0%, moderately above the high end of the Fed funds target range and implying that a rate hike may be near.

The concern is that the recent pickup in headline inflation will soon force the Fed’s hand and trigger one or more rate hikes to offset renewed pricing pressure. The case for rate hikes has been debatable, even after the inflation jump triggered by the conflict in the Middle East. TMC Research’s Fed Funds Model has estimated policy as moderately tight, offering a degree of inflation‑fighting medicine. But that mildly hawkish bias has continued to fade in recent months and is now essentially neutral, leaving the Fed vulnerable if inflation holds at current levels or rises further.

Several measures of inflation have jumped in recent months, driven by the Middle East supply shock that has lifted energy prices. The year‑over‑year change in the Consumer Price Index (CPI) rose to 3.8% through April — a three‑year high and substantially above the 2.4% pre‑war pace in February. Core CPI, which strips out food and energy and is a more reliable measure of underlying inflation, is also edging up but remains considerably softer at 2.7%. In both cases, inflation is running hotter than the Fed’s 2% target.

Warsh’s preferred measure of inflation, by contrast, suggests that inflation is lower and stable, giving the Fed chair more leeway to argue that rate hikes are premature. In his Senate confirmation hearing in April, he said he favors “trimmed” inflation measures, explaining that they offer better signals of underlying trends.

The Dallas Fed’s Trimmed Mean Personal Consumption Expenditures (PCE) Index, for example, rose 2.4% for the year through April, unchanged from March and only slightly higher than February’s pace.

Critics push back by noting that the trimmed‑mean PCE Index was slow to react to the 2021–2022 inflation spike, and so relying on this alternative measure could set the Fed up for another delayed reaction that gives pricing pressure room to run.

The Cleveland Fed’s inflation nowcast, however, suggests the current inflation run may be peaking. Headline CPI is expected to ease modestly in June to a 3.9% year‑over‑year rate, down from a projected 4.2% increase in the upcoming May report. Core CPI, meanwhile, is on track to hold steady at 2.8%.

The question is how the 12 members of the FOMC interpret the data. The focus on June 17 will be on the first among equals for policy votes — Warsh — who gives his first press conference as Fed chair that afternoon.

His preference for trimmed‑mean inflation will be under scrutiny, and will likely be subject to questions from the press. How he defends that preference under the glare of a live press conference will offer the first real clue about the kind of Fed chair he intends to be.