Fed Chair Warsh Sounds Hawkish as Fed’s Policy Bias Quietly Turns Dovish

By James Picerno | The Milwaukee Company

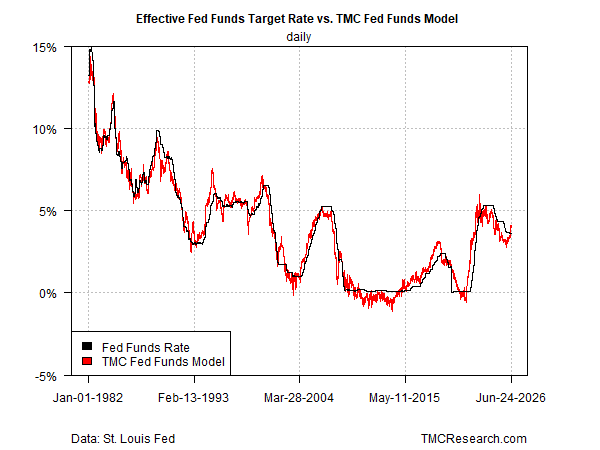

Fed stance has slipped into a dovish bias as our neutral rate estimate rises

Rising inflation pushed the model’s neutral rate higher

Fed funds futures are pricing in higher odds of rate hikes

Fed Chair Kevin Warsh struck a hawkish tone at his debut press conference last week, but the central bank’s policy stance has turned dovish in recent days, according to TMC Research’s Fed model.

For the first time in three years, the Effective Fed Funds Rate has fallen below our estimate of the neutral level of the Fed’s target rate—a gap that suggests monetary policy has shifted to a dovish bias (roughly 40 basis points below neutral as of June 24).

It’s important to understand the mechanics behind the shift. The Effective Fed Funds Rate has been unchanged since the Fed cut rates in December 2025. What has changed is one of the inputs to our model: inflation via the Consumer Price Index. The recent rise in CPI has pushed our estimate of the neutral rate higher.

The key takeaway: the Fed’s policy bias appears to have moved from moderately tight to moderately loose—not because of any new action by the central bank, but because of its lack of action in the wake of hotter prices.

The debate is whether the recent upturn in inflation will prove temporary, which would ease pressure on the Fed to tighten policy through one or more rate hikes. The risk is that stronger pricing pressure persists. If so, the longer the Fed waits to respond, the greater the possibility that inflation becomes more entrenched—forcing the Fed to raise rates higher and keep them elevated longer than would have been necessary with earlier action.

Warsh refrained from offering forward guidance at last week’s meeting, but almost half of the Fed’s members of the Federal Open Market Committee project at least one rate hike by year‑end, and several believe multiple increases may be needed.

Although Warsh has been critical of the Fed’s forward‑guidance efforts—such as publishing rate forecasts by FOMC members—he emphasized that “the Committee will deliver price stability.” He also noted that “inflation has been running well ahead of the Fed’s long‑stated inflation goal of 2%—that’s been going on for more than five years. Persistently high prices are a burden for the American people.”

The uncertainty is whether the Fed will soon raise rates or continue a wait‑and‑see approach that assumes the recent rise in inflation is temporary. The sharp drop in oil prices over the past several weeks—driven by what appears to be an end to the war with Iran—supports the view that headline inflation may have peaked and could soon ease.

Fed funds futures are pricing in roughly a 72% probability that the Fed will leave its target rate unchanged at next month’s FOMC meeting. For September, the probability rises to 87% for either no change or a cut.

The bond market also appears to be giving the Fed more room to be patient, if not implicitly assuming the inflation surge will prove transitory. The 10‑year Treasury yield, for example, has pulled back from its mid‑May spike, trading around 4.40% versus nearly 4.70% a month ago, although the current yield is still up sharply relative to where it began, just below 4.0%, on the eve of the war’s start.

The Fed’s next move is uncertain, but the window for inaction is getting narrower by the day. At some point soon, the inflation data will force a decision, one way or the other.