Cut or Hold? Fed’s December Decision Hangs On A Divided Outlook

By James Picerno | The Milwaukee Company

Markets have turned mixed on the rate-cut outlook as the Fed struggles to parse inflation and payrolls data

Fed officials appear split on the next move, as some call for caution while others warn against overtight policy.

Private payroll estimates point to labor market cooling, filling the gap left by October’s missing government data

The recent confidence in markets that the Federal Reserve will cut interest rates again in December is fading. The doves are driven by recent data that points to a weakening labor market, but some Fed officials are now expressing caution for another round of easing.

Boston Fed President Susan Collins, for example, expressed reluctance for lowering the target rate again at the December 10 policy meeting.

Atlanta Federal Reserve President Raphael Bostic on Wednesday said he favors leaving rates unchanged in December, explaining that “clear evidence” is still needed to confidently say that inflation is on a path of falling closer to the Fed’s 2% target.

A new poll by Reuters, by contrast, reports that 80% of economists predict the Fed will lower its target rate next month. Meanwhile, the policy-sensitive 2-year Treasury yield continues to offer an implied rate-cut forecast by trading well below the current Fed funds target rate.

But the Fed funds futures market is now pricing in a coin flip for next month’s rate decision.

One reason to reserve judgement on the next policy move is tied to the outlook for inflation: “Annualized month-over-month growth rates shows that 55% of items in the CPI basket are growing faster than 3%,” according to analysis by the chief economist at Apollo Capital Management.

The case for cutting continues draws much of its support from recent updates that show that hiring at companies remains soft. Filling in for the government’s missing payrolls data for October, courtesy of the shutdown, markets focused on the downshift in the labor market last month, based on estimates by ADP and Revelio Labs.

Federal Reserve Governor Stephen Miran recently argued that another rate cut is needed in December to lower US recession risk. “If you keep policy this tight for a long period of time, then you run the risk that monetary policy itself is inducing a recession,” he told The New York Times. “I don’t see a reason to run that risk if I’m not concerned about inflation on the upside.”

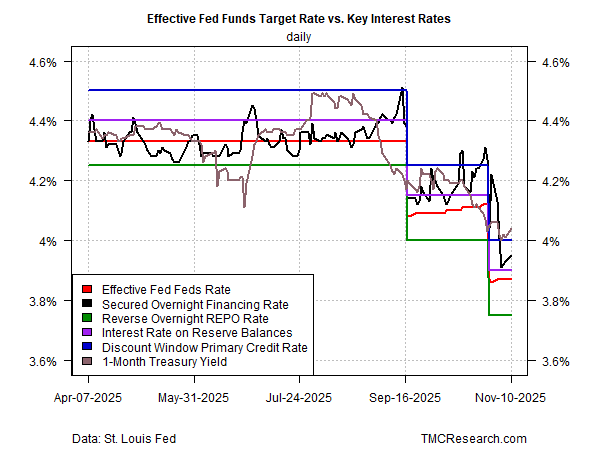

A useful compliment for monitoring if market conditions agree, or not, is tracking how the Fed policy channel is evolving, based on various key interest rates that are proxies for assessing the near-term outlook. The chart below highlights that the effective Fed funds rate (red line) remains essentially at the mid-point of the channel, which reflects a neutral bias (for data through Nov. 10).

For context on what a clear hawkish bias looks like, consider how rates stacked up shortly ahead of the rate-hiking cycle that started in March 2022, when the 1-month Treasury yield quickly rose from the bottom of the channel to the upper range.

On that basis, the market may be starting to price in, if not a rate hike, a rate pause. Per the first chart, the 1-month Treasury yield is now defining the highest rate for the channel. If this persists, the case will strengthen for expecting the Fed to hit the pause button next month.