A Final Powell Pause at the Fed as Inflation Risks Rise

By James Picerno | The Milwaukee Company

Markets expect the Fed to hold its target interest rate steady, but inflation risk from the energy shock is rising

Bond yields are edging higher, hinting at early pricing of renewed inflation pressure

Powell’s final meeting comes as Warsh prepares to take over amid growing policy uncertainty

Markets are pricing in a near-certainty that the Federal Reserve will leave interest rates unchanged at Wednesday’s policy meeting, but the high‑confidence forecast for standing pat belies the challenges that lie ahead for the central bank.

The main uncertainty that will lurk over policy decisions in the months ahead is the threat of higher inflation triggered by the supply‑side energy shock that’s reverberating from the Middle East conflict.

Fed funds futures are betting that the path of least resistance is to do nothing, for tomorrow and beyond. The implied odds for policy through the end of the year favor keeping the Fed’s target rate steady at 3.50% to 3.75%. The question is whether that’s a reasonable forecast if inflation pressures continue to build due to elevated energy prices.

The effects of the war are already conspicuous in the March report for the Consumer Price Index (CPI), which shot up to a 3.3% annual increase—a sharp change from 2.4% in February. Markets are bracing for a repeat performance in the April update, and possibly an even higher pace, in the wake of an ongoing shutdown of energy exports from the Middle East.

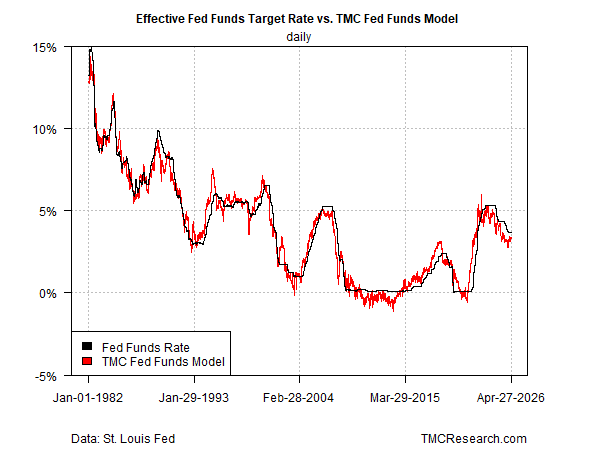

TMC Research’s Fed Funds Model still estimates that the policy stance is modestly tight, which may give the central bank cover to argue that leaving rates steady is reasonable while inflation concerns linger. But as today’s update of the model shows, the hawkish bias has faded lately. The current reading indicates that the actual Effective Fed Funds Rate is roughly 35 basis points above the estimated optimal level for the target rate. That’s near the lowest degree of hawkish tilt in more than a year — far below the 120‑basis‑point spread as recently as September 2025.

The argument in favor of doing nothing at tomorrow’s Fed meeting—and for some time after—is that the inflationary effects of the war (and the subsequent stalemate that’s restricting Gulf energy exports) are unclear. Although most forecasters expect higher inflation in the near term, economists are debating how long the run‑up in pricing pressure will last, and how forcefully the Fed should react, if at all.

The risk is that the central bank repeats the mistake of responding too slowly to the 2021–2022 inflation spike. Critics are quick to note that even before the war with Iran started on Feb. 28, the Fed hadn’t fully repaired the damage from the previous price surge, as shown by year‑over‑year inflation running above the 2% target in recent years.

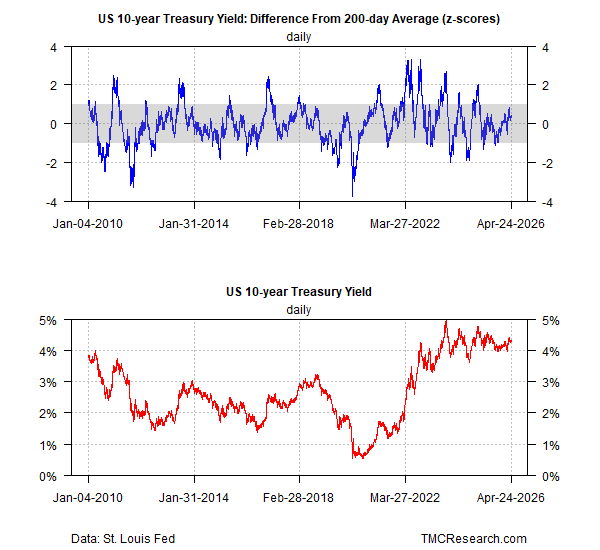

But if inflation risk is rising, presumably the bond market would be reacting by demanding a higher yield premium. Treasury yields have increased since the conflict started, but the increase has been moderate and has yet to break decisively higher.

The benchmark 10‑year yield, for example, continues to trade in a middling range relative to the past year or so, closing at 4.35% as of Monday’s close. But as the chokehold on Middle East energy exports continues, inflation pressure is still on a path to rise.

One sign that the bond market is beginning to price in elevated inflation risk: the 10‑year yield trades close to the upper range of one standard deviation from the mean for the current rate vs. its 200‑day average. For now, the 10‑year rate is holding in a “normal” range, indicated by the grey zone in the chart below. If the market lifts the benchmark rate closer to the upper level of this range, that shift would suggest that investors are becoming anxious.

An added twist: tomorrow’s decision on interest rates will be the last for Fed Chair Jerome Powell, whose term ends next month. His pending replacement, Kevin Warsh, is back on track for confirmation after Republican Senator Thom Tillis on Sunday ended his opposition to the nominee. Because of the GOP’s thin 13‑to‑11 majority on the Banking Committee, Tillis’s vote is crucial to advance a vote on Warsh to the full Senate.

Warsh is expected to push for rate cuts after he takes the helm at the Fed next month, or so his recent comments suggest. But with surging energy costs threatening to keep inflation higher for longer, it’s unclear if he can persuade enough hawks at the Fed to ease rates and potentially create conditions that lead to another policy mistake.

For now, the Fed can stand still; the question is whether the economy will let it in the months ahead.