A $3 Trillion Question: How Fragile Is Private Credit?

By James Picerno | The Milwaukee Company

Redemptions are rising and managers are starting to limit withdrawals

Software‑linked lending is flashing stress signals

A sharp jump in Treasury yields could trigger more outflows

Private credit has gone from a niche backwater to an increasingly mainstream allocation, but investors are discovering that its headline attraction — lofty yields — may come with real, often underappreciated risk.

Minds have become more focused on the risk aspect lately as questions about the viability of the market come under critical scrutiny. In years past, worries about private credit could be ignored by most investors, but the industry for lending by private equity firms has boomed, especially in the post‑pandemic years. Critics are now asking whether this former backwater is becoming too big to fail and poses a threat to the wider economy.

The value of debt financing beyond conventional borrowing channels (banks and the bond market) in the US was $1.34 trillion in 2024, roughly five times higher than in 2009, according to the Federal Reserve. Some estimates now peg the figure above $3 trillion-plus in 2026.

A Boom That’s Finally Drawing Scrutiny

Few observers saw the growth of alternative lending sources as a problem until recently, when investor redemptions began rising sharply, persuading some managers to limit withdrawals. One trigger for turning cautious on private credit is the industry’s hefty lending to software companies, which have come under pressure lately on the view that artificial intelligence threatens their business models.

Right or wrong, a more cautious view on the outlook for software firms is reverberating back into private credit. The fear is that a stress‑driven correction in private credit, given its breadth and depth in the financial ecosystem, could create a liquidity shock on Wall Street and beyond.

Some analysts point to rising stress signals, such as an increasing default rate among US private‑credit borrowers. But in a sign that the worst may have passed, Fitch Ratings estimates that the default rate in US private credit declined to 5.4% in February, down from January’s 5.8%, the highest since August 2024.

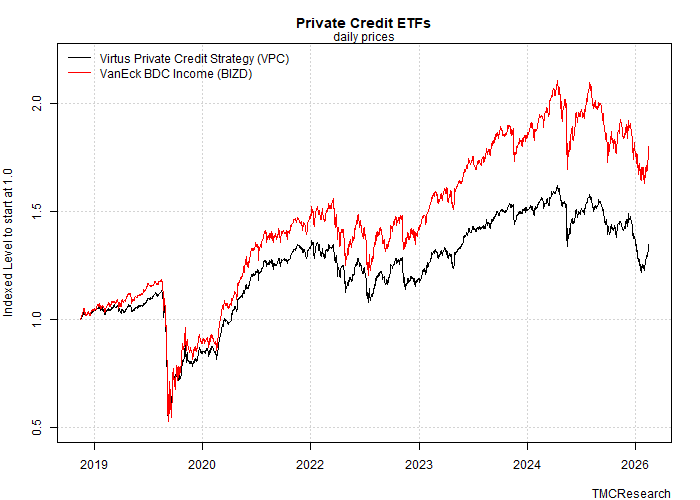

Even if you never touch private credit, the industry is worth tracking because stress in this opaque corner of the market can transmit outward — through bank funding lines, credit spreads, and real‑economy financing — and turn a niche disruption into broader financial and economic strain. A useful starting point for monitoring sentiment is watching two ETFs that have been plying these waters.

The funds in the chart below represent two measures of the private‑credit industry. The Virtus Private Credit Strategy ETF (VPC) tracks the Indxx Private Credit Index, which is composed of US‑listed business development companies (BDCs) and closed‑end funds (CEFs) focused on private credit. The VanEck BDC Income ETF (BIZD) targets the MVIS US Business Development Companies Index, a proxy for the performance of publicly traded BDCs, which are funds that invest in small- and mid-sized companies.

Note the recent upturn in both funds, which may be a sign that the market is beginning to look through the recent turbulence. Some high‑profile observers of the market appear to be softening concerns about the risk outlook. JPMorgan Chase CEO Jamie Dimon said this week that he’s “not particularly worried” about his firm’s $50 billion allocation to private credit.

The Signals That Could Matter Most For Private Credit

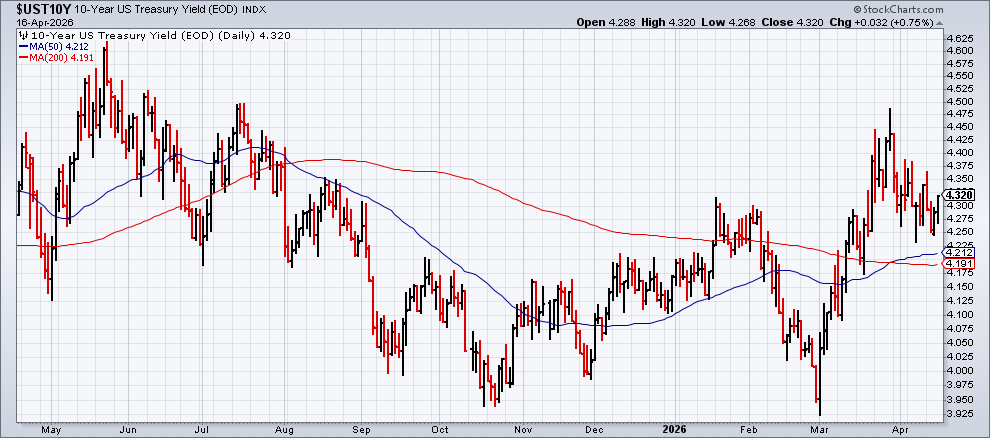

A rise in interest rates could change minds, but here too the latest numbers suggest the market has steadied. The 10‑year Treasury yield, for example, has increased moderately since the start of the war with Iran, but the current 4.32% yield remains in a middling range for the trailing one‑year period. A rise above the recent peak (roughly 4.45%) could be a new warning sign.

Perhaps the critical variable is when — or if — banks dramatically pull back their credit lines, a source of liquidity that has been instrumental to date in financing new deals and managing cash flow. Those lines of credit may come under closer scrutiny if more investors try to liquidate their private‑credit holdings.

What might trigger a new round of investor withdrawals? There are many possibilities, but a sharp rise in Treasury yields is near the top of the list. That scenario may become more plausible if incoming inflation data is hotter than expected due to the supply‑side energy shock unleashed by the war.