60/40 Portfolio's Reported Death Is Greatly Exaggerated

Bear markets tend to bring out dark forecasts, especially of the variety that insists: “It’s different this time.” It would be naive to argue that nothing changes in financial markets or economics. Au contraire – markets and economies, like all realms of the social sciences, are constantly evolving. Investing, in short, isn’t physics.

But while there are no genuinely unchanging rules on Wall Street on par with gravity and the second law of thermodynamics, there are some time-tested truisms that equate with received wisdom – wisdom that should be dismissed rarely, if at all. A card-carrying member of this club is the view that holding a mix of stocks and bonds is a building block for a diversified portfolio of stocks and bonds that earns solid risk-adjusted returns.

Yet even core principles of finance periodically fall on hard times. Unsurprisingly, during the recent bear market in bonds there was a bull market in claims that the traditional equities/bonds building block was on its deathbed. The standard reference point is the so-called 60/40 portfolio, a widely used benchmark for monitoring a simple asset allocation strategy. After several decades of strong performance, the 60/40 mix ran into trouble recently when the Federal Reserve began raising interest rates in March 2022. The rapid series of hikes took the wind out of bonds, which suffered one of their worst periods in history in 2022-2023. The sharp loss inspired more than a few pundits to declare that the 60/40 portfolio was dead.

With the benefit of hindsight, it’s now clear that while the 60/40 strategy has suffered, it’s proven resilient once more. Year-to-date through the end of the third quarter, the 60/40 portfolio is up 14.5%. Granted, most of that is due to the equity allocation. But bonds have been rebounding since May and currently are up 3.7% year to date. Factoring in the potential for fixed income to minimize the downside volatility in stocks through time, the price tag for the risk-management aspect of bonds is looking more attractive these days.

The revival of the bond market suggests that the previous rush to judgment – a hardy perennial on Wall Street – has proved to be premature once again.

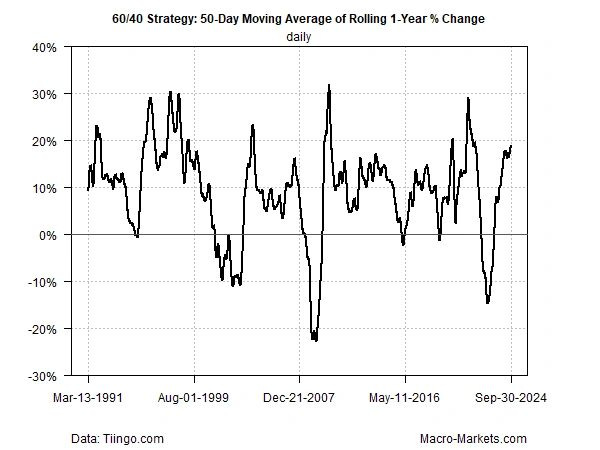

Consider the history of the 60/40 portfolio on a rolling 1-year basis since 1991 (the results are smoothed with a 50-day moving average to highlight the trend’s evolution). Using a set of Vanguard index funds as proxies for US stocks (VFINX) and bonds (VBMFX) indicates that while the strategy suffered recently, the decline wasn’t unprecedented. Nor was the relatively rapid and robust recovery. As of September 30, the 50-day average of the 60/40 portfolio is approaching a 20% year-over-year advance.

The basic allure of the 60/40 mix remains intact, namely: generating a substantial portion of an equities-only return with significantly less risk. Using the latest numbers reconfirms this central point. Consider: since 1990, the 60/40 portfolio earned roughly 83% of the stock market’s performance with only 58% of the risk (based on standard deviation of daily returns). The results degrade a bit for performance when measured over the past ten years: the 60/40 portfolio earned 66% of the stock market’s return but with only 59% of the risk. Still, the risk-reward profile still looks attractive as a baseline strategy.

Critics say that the bond market in the years ahead faces headwinds that were absent over the past three decades. Interest rates are no longer in a generational decline in the wake of the dramatic spike in the early 1980s. That may be true, but it’s not obvious that it’s time to write the 60/40’s obituary.

For starters, the 60/40 mix is a benchmark that can and should be customized for investors, depending on risk tolerance, time horizon and other factors. That implies that a 60/40 allocation can be lowered to 50/50 for some clients or raised to 70/30 for others. In addition, the bond component can be revised by shortening or lengthening duration, or adding securities beyond the US investment-grade fixed-income landscape. Commodities, real estate and other asset classes and trading strategies are also possible inputs to consider diversifying bonds and stocks.

Asset allocation, in other words, can move beyond a simple 60/40 portfolio in multiple dimensions. At the same time, it’s crucial to recognize that a 60/40 benchmark has been and will probably remain a competitive benchmark for asset allocation strategies generally.

Meantime, the mistake that too many pundits made in declaring the 60/40 dead was confusing a market cycle with a permanent regime shift. As J.P. Morgan famously remarked when asked for a forecast: Markets will continue to fluctuate. Assuming that this empirical truism automatically leads to an asset class’s death is assuming too much.